California’s New Auto Insurance + Roadway Laws in 2025: What Every Driver Needs to Know

December 11, 2024 | Article by Chain | Cohn | Clark staff Social Share

California in 2025 is set to implement new laws and changes that will directly impact drivers, insurance policies, and accident-related claims.

Starting in January, California is increasing its minimum auto insurance liability limits for the first time in over 50 years, ensuring better financial protection for accident victims. While this change promises more comprehensive coverage, it also means drivers may see higher premiums and new responsibilities to stay compliant.

For law firms like Chain | Cohn | Clark, which specialize in accident and injury cases, understanding these changes is crucial to helping clients. Learn more about the new laws going into effect in 2025 and their implications.

===

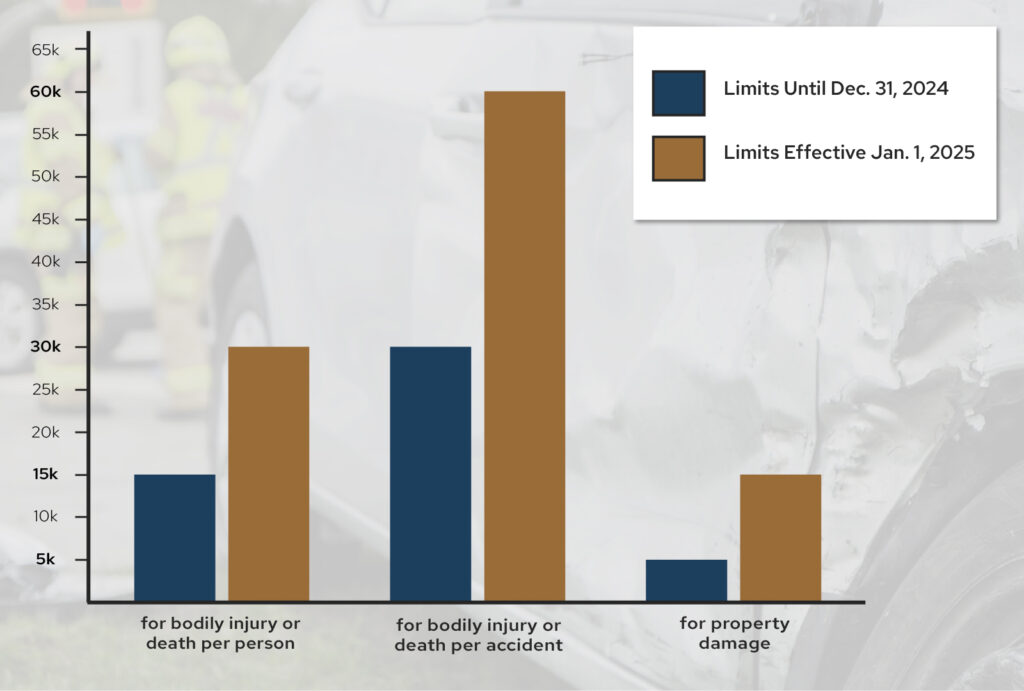

NEW AUTO INSURANCE LIABILITY LIMITS

One of the most impactful changes for California drivers in 2025 is the increase in minimum auto insurance liability limits under Senate Bill 1107, also known as the Protect California Drivers Act. This adjustment marks the first increase in over 50 years and aims to provide better financial protection for accident victims. Here’s a breakdown of how limits will change:

- Limits Until Dec. 31, 2024:

- $15,000 for bodily injury or death per person

- $30,000 for bodily injury or death per accident

- $5,000 for property damage

- Limits Effective Jan. 1, 2025:

- $30,000 for bodily injury or death per person

- $60,000 for bodily injury or death per accident

- $15,000 for property damage

Under the new limits with a minimal policy, an insurance company will pay out no more than $30,000 to any individual injured and no more than a total of $60,000 for an accident no matter how many people are injured. The increase to $60,000 on the per accident limits will make it much more likely that in cases involving multiple injured parties that a fair settlement can be obtained.

Advocates say the previous limits were established decades ago and are no longer sufficient to cover the rising costs of medical care and vehicle repairs. By doubling the liability limits, California aims to ensure that accident victims can recover more adequate compensation for their injuries and damages without facing significant out-of-pocket expenses

“Raising California’s auto insurance liability limits is a long-overdue step toward justice for accident victims,” said Doug Fitz-Simmons, attorney at Chain | Cohn | Clark, who has more than 30 years of experience working with insurance companies on accident and injury cases. “No one should be left drowning in medical bills or repair costs because outdated policies failed to provide adequate coverage.”

IMPLICATIONS

As an illustration, the following example compares a policy limit settlement under the current and the new law:

In a case where a injured person has $8,000 in medical bills and has retained an attorney on a contingency basis of 33-1/3% — the standard rate — a typical $15,000 policy limit settlement may result in the following allocation:

- Reimbursement of Medical Expenses: $8,000

- Attorney’s Fees: $5,000

- Client Net: $3,000

In a case where a injured person has $8,000 in medical bills and has retained an attorney on a contingency basis of 33-1/3%, a typical $30,000 policy limit settlement may result in the following allocation:

- Reimbursement of Medical Expenses: $8,000

- Attorney’s Fees: $10,000

- Client Net: $12,000

The increase in policy limits will make a significant difference to injured people in being able to recover more compensation in cases where the party responsible has a minimal policy limit. Furthermore, the increases in bodily injury limits will benefit the at-fault party by reducing the potential that someone with a minimal policy limit that causes an accident may be personally responsible for damages over the policy limits coverage.

Among the implications of higher limits are:

- Higher Premiums: Insurance providers will adjust their rates to reflect the increased coverage requirements. Drivers with minimal coverage policies may see a noticeable rise in premiums. It may come as a surprise to many consumers that California currently ranks in the 10 lowest average insurance automobile rates. This will certainly go up as the minimal limits are being doubled.

- Enhanced Protection: The new limits will reduce the financial burden on accident victims and minimize situations where medical bills or repair costs exceed policy coverage.

- Compliance Necessity: Drivers with policies below the new minimums must update their coverage by Jan. 1, 2025, to avoid penalties.

California still has no state requirements to maintain uninsured motorist bodily injury (UMBI) coverage. This type of coverage is an option for policyholders to purchase with the liability insurance. This coverage provides insurance to compensate for injuries and damage caused by an uninsured driver. The underinsured coverage takes effect when an injured party’s injuries and damages value exceeds the responsible party’s insurance coverage. With approximately 17% of California drivers uninsured, UMBI coverage provides an essential safety net for responsible motorists.

Higher liability limits mean that injured parties may recover more substantial settlements from at-fault drivers’ insurance policies. Additionally, victims of serious accidents will be less likely to face out-of-pocket expenses for medical bills or vehicle repairs. Lastly, as insurance premiums rise, disputes over fault and coverage may also increase, leading to more litigation.

The legislative updates reflect California’s acknowledgment of inflationary pressures in healthcare and auto repair industries:

- Medical costs associated with car accidents have risen significantly over recent years.

- Vehicle repair expenses have also surged due to advancements in technology and labor costs

These factors have made it increasingly difficult for accident victims to cover expenses under outdated liability limits. The new laws aim to bridge this gap by ensuring more comprehensive financial protection.

COMPLIANCE

So, what should drivers do as a result of the change? To ensure compliance with these new laws and avoid penalties:

- Make Sure You Have Coverage: It is the driver’s responsibility to make sure that they meet the financial responsibility requirements. If you are driving someone else’s car, you must make sure that there is coverage on the vehicle and that you are a permissive driver or that you have your own insurance coverage.

- Review Your Current Policy: Check whether your existing auto insurance policy meets or exceeds the new minimum requirements.

- Contact Your Insurance Provider: If your policy falls short of the new limits, update it before Jan. 1, 2025.

- Consider Additional Coverage: While meeting the minimum requirements is mandatory, opting for higher coverage can provide even greater financial security.

- Underinsured/Underinsured Motorist Coverage: Consider obtaining underinsured/underinsured motorist coverage to best protect yourself, and your family.

- Explore Discounts: To offset rising premiums, inquire about discounts for safe driving records or bundling policies

The importance of being insured is significant. If you are involved in an accident that is not your fault and you are uninsured, there are serious consequences. Under Proposition 213, you can only recover special damages (out of pocket losses such as medical bills and loss of earnings). You cannot recover for pain and suffering damages by law. Further driving without insurance can result in fines, driver’s license suspensions, and potentially the vehicle being impounded.

It is also important to understand that an injured party does not have to accept a policy limit offer from an insurance company. If an insured driver that causes an accident with the value of the injuries in excess of the policy limits, they could be liable for the amount of any judgment exceeding the insurance policy limit.

Currently California has a high rate of uninsured drivers on the roadways. With the anticipated increase in premiums, there will certainly be an increase in the number of uninsured drivers. This is why it is increasingly important to have uninsured motorist coverage. Many people injured in accidents are angry when they find out the at-fault driver was not insured and the likelihood of collecting a recovery from the uninsured driver is minimal. The best way to protect against that situation is having uninsured motorist coverage.

While these changes primarily focus on financial accountability after accidents, they also align with broader efforts to improve roadway safety across California. By ensuring adequate insurance coverage for all drivers, the state seeks to reduce instances where victims are left uncompensated after accidents. The adjustments encourage responsible driving behavior by emphasizing financial accountability.

HISTORY OF LIMITS

In 1974 the California Legislature enacted laws that required that anyone who owns or operates a motor vehicle in the State of California must be capable of providing monetary protection to people who may be injured or suffer property damage as a result of a traffic collision. There were four ways that the proof of financial responsibility could be met, with the most common being proof of a liability insurance policy with a company authorized to do business in California. In 1974, the minimum coverage required $15,000 for bodily injury or death per person, $30,000 for bodily injury or death per accident, and $5,000 for property damage.

Those limits remained the same until the new legislation was passed that takes effect on Jan. 1, 2025. To help demonstrate the ineffectiveness of the old limits to adequately compensate insured persons, consider the average inflation from 1974 to 2024 was 3.78% per year. According to the Bureau of Labor Statistics consumer price index, one dollar today can only buy 15.625% of what it could in 1974. This significantly reduces both the dollar amount an injured person might recover after paying medical bills, and the value of the pain and suffering damages recovered. For example, $3,000 in medical bills in 1974 would cost over $18,000 today based on the inflation index. Many people do not realize that a personal injury settlement has to reimburse medical costs through Medicare, MediCal, private insurance, or lien treatment. One of the services our firm provides is at the conclusion of the case to negotiate the amount of the reimbursement.

Due to minimal limits remaining in effect of 50 years, an individual injured by another at-fault driver often was often inadequately compensated for their injuries due to the increased cost of medical care and the increase in other losses, such as higher loss of earnings due to higher wages compared to 1974.

Until the changes in 2025, California remains in comparison among the lowest in the United States, joining only two other states with minimal liability limits of $15,000/30,000. Two other states have Personal Injury Protection laws which are no-fault coverages that are $15,000 per individual or less. The legislation will bring California to a level more consistent with other states.

Approximately 60% of the states have minimal limits of $25,000 per individual and $50,000 per accident. Most other states increased the minimal limits long before California enacted higher financial responsibility laws. This increase will place California in the top 20% in comparison to other states’ insurance minimal limits. The changes being made by the California Legislature will help address the changes necessary to better compensate injured people due to accidents caused by other drivers.

As for other new laws in 2025 affecting road safety and injured workers (another practice area for Chain | Cohn | Clark) …

===

‘DAYLIGHTING’

Assembly Bill 413 prohibits both personal and commercial vehicles from parking or stopping within 20 feet of any marked or unmarked crosswalk anywhere in the state. The law applies to curbs whether they’re red striped or not.

The new law is an effort to make roads safer for pedestrians and cyclists. Though it has technically been in effect since the start of 2024, cities can start fining drivers starting Jan. 1. It is nicknamed the “daylighting” law because vision is better in the daylight.

Fines will vary by jurisdiction. In San Francisco, fines will start at $40 per violation.

“AB 413 saves lives through a simple and effective solution to improve road safety,” said Assemblymember Alex Lee, who authored the bill, in a statement. “Intersections are some of the most dangerous portions of our roads, and daylighting will make them safer for everyone. More than 40 states have already implemented daylighting laws prior to AB 413, and I’m glad that California is joining the rest of the country on improving road safety.”

===

CALIFORNIA WORKER BENEFITS

Senate Bill 1105 by Sen. Steve Padilla, D-Chula Vista, allows agricultural workers to use paid sick days for preventive care, in the event that extreme heat, smoke or other natural hazards would make working outdoors dangerous. Newsom vetoed, however, a bill that would have allowed farmworkers to file worker’s compensation claims for heat-related illnesses suffered while working.

“California farmworkers put their bodies through incredible stress every day to feed families across the globe,” said Senator Padilla in a statement. “This law is critical as we adapt our policies to the impacts of climate change. Giving these workers the freedom and peace of mind to use their hard earned sick days to protect their health further adds to California’s landmark labor protections.”

LEMON LAW CHANGES

Starting Jan. 1, California’s “lemon law” will undergo significant changes under Assembly Bill 1755, aimed at streamlining the resolution of disputes over defective vehicles but raising concerns about reduced consumer protections. Key updates include:

- Written Notice Requirement: Consumers must now notify manufacturers in writing (via letter or email) about vehicle defects to pursue buybacks or replacements.

- Manufacturer Response Deadlines: Automakers must respond within 30 days and complete buybacks or repairs within 60 days, or face penalties of $50 per day for delays.

- Statute of Limitations: Claims must now be filed within six years of purchase or one year after the warranty expires, whichever comes first.

- Streamlined Litigation: New rules expedite mediation and discovery processes for lemon law lawsuits.

While proponents argue these changes will reduce court backlogs and speed up resolutions, critics warn they may weaken protections for consumers, particularly for used vehicles. A recent California Supreme Court ruling clarified that manufacturers are not required to honor warranties on resold vehicles, further complicating the landscape. Consumers are advised to consult legal experts to navigate these changes and protect their rights.

23ABC News in Bakersfield spoke with Chain | Cohn | Clark attorney Juan Garza about the changes.

———

If you or someone you know is injured in an accident at the fault of someone else, or injured on the job no matter whose fault it is, contact an experienced accident attorney at Chain | Cohn | Clark by calling (661) 323-4000, or fill out a free consultation form, text, or chat with us at chainlaw.com.

———

MEDIA COVERAGE

- New California Auto Insurance Laws Increase Minimum Coverage for Drivers in 2025 (23ABC News — Jan. 7, 2025)

- Abogado Juan Garza de Chain | Cohn | Clark Habla Sobre Nuevos Requisitos de Seguros de Auto (Telemundo Bakersfield – Jan. 1, 2025)

- New auto insurance law to require higher liability limits for CA drivers (Bakersfield Eyewitness News – Dec. 12, 2024)